At MOSTA's OFIC Module 2, we just had a great line-up of speakers and a good panel session.

Ms Sanya Reid Smith of Third World Network drew our attention to domestic agriculture subsidies remaining in places like the US and EU within the trade agreement contexts, Malaysia's bounded export duty (up to 8.5% on CPO)exemption under TPPA (and RCEP leaked documents showing Japan and South Korea asking for zero), that IP extensions may reduce availability of non-patent agricultural chemicals (that often result in prices being 3x higher), and TPPA's potential impact on procurement by federal government entities and large SOEs, ILO labour standards becoming enforceable, and question whether palm oil milling is a service and therefore subject to liberalisation. The USA certification process for TPPA may add more requirements (beyond the text, with topics as yet unknown), and that many countries wait until the USA proceeds before making changes to domestic laws and regulations. She offered a thorough applied analysis of TPPA on palm oil that has not featured in previous public for a.

Dr Joe Feyertag of LMC International Ltd explained a profound shift in grain and vegetable oil production post 2002 with large production and acreage growth amidst the biofuels boom, rapid meat consumption transitions, oil palm expansion less than a quarter of maize and soy acreage expansion, the 2010s being the end of the biofuels decade and rise of the protein decade, future growth scenarios showing a hypothetical moratorium on palm oil volume resulting in even larger increase in soy acreage likely in the Amazon Basin, a look at US biodiesel market volume, potential volume return from Argentina and Indonesia and EU biofuels policy news of no more public support for food-based feedstocks from 2020. He concluded that environmental aspirations need to take a more nuanced consideration of how demand drives expansion across the vegetable oil complex (palm, soy, rape/canola and sun), and for GMO products.

Mr James Caffyn of Gira Strategy Consultants provided major insights into vegetable oils usage in the dairy sector - specifically analog cheese, fat-filled milk powders, growing-up milk and infant formula - with great data on dairy-veg oils price arbitrage of over 4.5x, market size and growth, vegetable oil inclusion ratios and palm oil tonnage indicators (over 1.5 million tonnes in FFMP and GUM-infant formula). What came strongly across for palm oil was the fast growth potential of this segment (especially in Asia), its technical proficiency, compelling price arbitrage, market perception, regulatory concerns and food safety.

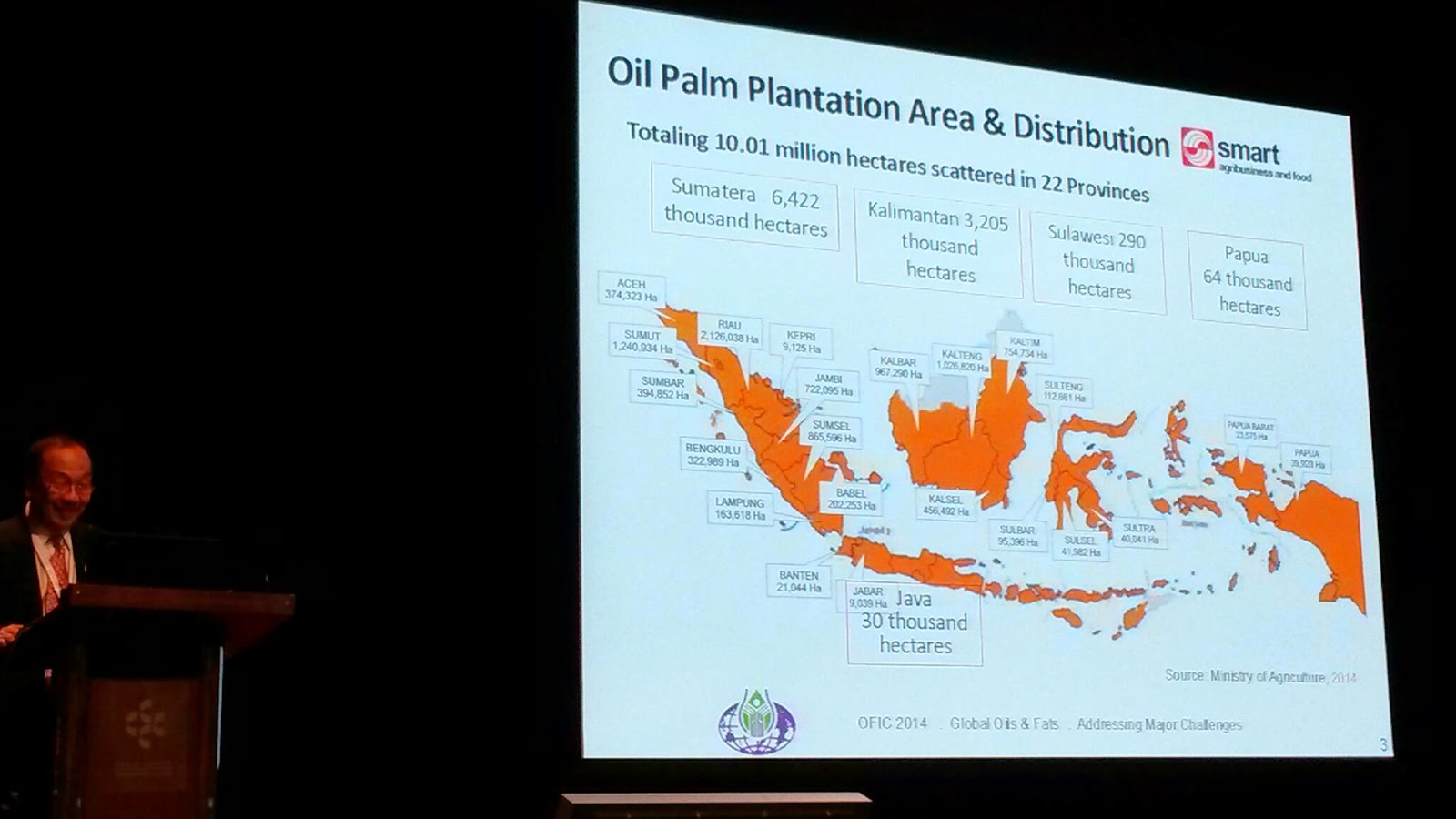

Mr Syahril Syazli Ghazali of Ministry of International Trade and Industry (MITI) of Malaysia offered wonderful insights into TPPA, as Lead Negotiator for the Market Access Chapter. 20% of Malaysia palm products go to TPPA countries and a focus was on Canada and Mexico on duty removals, Malaysia's ability to carve out export duties (bounded basis), and the need to comply to international standards will be a cost to Malaysia industry and government but it is the way forward.

In our panel discussion, we fielded a question on EFSA's 3MCPDE issue - the greater volume concern would arise if it also affects China dairy sector demand. As for biodiesel prospects, these are quite limited to Southeast Asia. Moreover sludge oil has been removed from double-counting and is unlikely to come back soon. From the floor, we heard from MR Chandran on the problem of definitions of by-products versus waste products, and that freedom of association for labour will be an issue especially since 30-35% of production cost is labour (Sanya mentioned PWC's report finding that one week stoppage could impact 2% of revenue). On my question about a pathway for palm to USA biofuels (beyond a handful of grandfathered facilities), Joe said that GHG emissions reductions is an official problem and Syahril clarified that USA biofuels access negotiation was tried but remains on the table without a solution via TPPA. To MR Chandran's added question on USA (California) market potential (this being a growth market versus EU not being seen as having much potential), I highlighted the change in the US Customs Border and Protection (CBP) rule against forced-labour imports in force since March 2016 and that it has already disrupted cargoes of tea and sweeteners; and it is notable that California leads in lawsuits on child labour allegedly in the cocoa supply-chain of large brand name companies. Sanya notes that the US CBP rule reinforces TPPA requirements and that complaints can be made against products and producers.

In conclusion, we covered the development and prospects for important fast-growing end-uses for vegetable oils and focussed on issues for Malaysia palm oil. Palm oil has a complex processing chain and a big range of applications. It has tremendous technical proficiency and price advantage in food uses, but if needs policy support in biofuel applications. Success in market share penetration is mediated by trade policy and new breed trade agreements (require upgrade to international standards in production and more). This affects relative price-cost and some non-price/non-tariff issues may also affect price-cost.

Photo: Mr Syahril at the rostrum by Khor Yu Leng

Ms Sanya Reid Smith of Third World Network drew our attention to domestic agriculture subsidies remaining in places like the US and EU within the trade agreement contexts, Malaysia's bounded export duty (up to 8.5% on CPO)exemption under TPPA (and RCEP leaked documents showing Japan and South Korea asking for zero), that IP extensions may reduce availability of non-patent agricultural chemicals (that often result in prices being 3x higher), and TPPA's potential impact on procurement by federal government entities and large SOEs, ILO labour standards becoming enforceable, and question whether palm oil milling is a service and therefore subject to liberalisation. The USA certification process for TPPA may add more requirements (beyond the text, with topics as yet unknown), and that many countries wait until the USA proceeds before making changes to domestic laws and regulations. She offered a thorough applied analysis of TPPA on palm oil that has not featured in previous public for a.

Dr Joe Feyertag of LMC International Ltd explained a profound shift in grain and vegetable oil production post 2002 with large production and acreage growth amidst the biofuels boom, rapid meat consumption transitions, oil palm expansion less than a quarter of maize and soy acreage expansion, the 2010s being the end of the biofuels decade and rise of the protein decade, future growth scenarios showing a hypothetical moratorium on palm oil volume resulting in even larger increase in soy acreage likely in the Amazon Basin, a look at US biodiesel market volume, potential volume return from Argentina and Indonesia and EU biofuels policy news of no more public support for food-based feedstocks from 2020. He concluded that environmental aspirations need to take a more nuanced consideration of how demand drives expansion across the vegetable oil complex (palm, soy, rape/canola and sun), and for GMO products.

Mr James Caffyn of Gira Strategy Consultants provided major insights into vegetable oils usage in the dairy sector - specifically analog cheese, fat-filled milk powders, growing-up milk and infant formula - with great data on dairy-veg oils price arbitrage of over 4.5x, market size and growth, vegetable oil inclusion ratios and palm oil tonnage indicators (over 1.5 million tonnes in FFMP and GUM-infant formula). What came strongly across for palm oil was the fast growth potential of this segment (especially in Asia), its technical proficiency, compelling price arbitrage, market perception, regulatory concerns and food safety.

Mr Syahril Syazli Ghazali of Ministry of International Trade and Industry (MITI) of Malaysia offered wonderful insights into TPPA, as Lead Negotiator for the Market Access Chapter. 20% of Malaysia palm products go to TPPA countries and a focus was on Canada and Mexico on duty removals, Malaysia's ability to carve out export duties (bounded basis), and the need to comply to international standards will be a cost to Malaysia industry and government but it is the way forward.

In conclusion, we covered the development and prospects for important fast-growing end-uses for vegetable oils and focussed on issues for Malaysia palm oil. Palm oil has a complex processing chain and a big range of applications. It has tremendous technical proficiency and price advantage in food uses, but if needs policy support in biofuel applications. Success in market share penetration is mediated by trade policy and new breed trade agreements (require upgrade to international standards in production and more). This affects relative price-cost and some non-price/non-tariff issues may also affect price-cost.